Alena Kravchenko/iStock Editorial via Getty Images

Expenditure Thesis

Google (NASDAQ:GOOGL) (NASDAQ:GOOG) reported its extremely anticipated FQ1 card on Tuesday (April 26) in a closely watched tech earnings period for the #1 leader in the digital ad current market. Snap’s (SNAP) current general performance showed that the headwinds have been manageable, despite the ongoing difficulties from the ad source chain and Apple’s (AAPL) ATT.

Google delivered a blended Q1 card that demonstrated toughness in model ads but slower progress in immediate response advertisements (warning to Meta (FB) later on today). Search adverts performance was solid, led by journey and retail, as world economies reopened. Nonetheless, YouTube’s underperformance was parsed by analysts on the phone. Notably, YouTube noticed solid engagement in shorts, even nevertheless monetization is not fairly ready, symbolizing a in the vicinity of-time period headwind.

Over-all, we like Google’s Q1 card, even with the near-time period headwinds from the Russia-Ukraine conflict and the disruptions from the advert provide chain. Having said that, there could be around-expression volatility. Management also guided to hard Q2 comps in advance, as it laps past year’s powerful functionality. Nonetheless, we feel GOOGL stock’s existing valuation had currently reflected these headwinds, investing effectively underneath its 5Y valuation averages.

We examine why GOOGL stock remains a Acquire after its Q1 card.

Google Noted A Mixed FQ1 Card

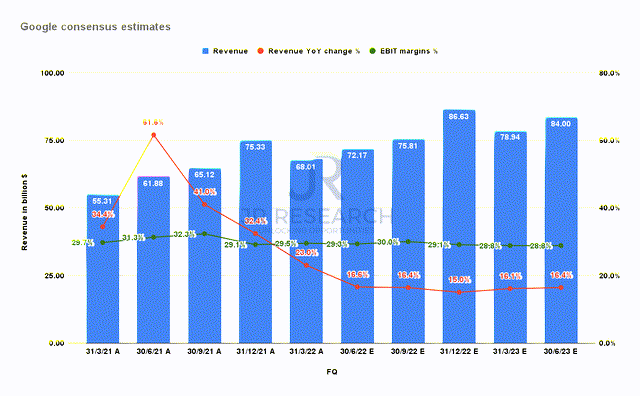

Google consensus estimates (S&P Money IQ)

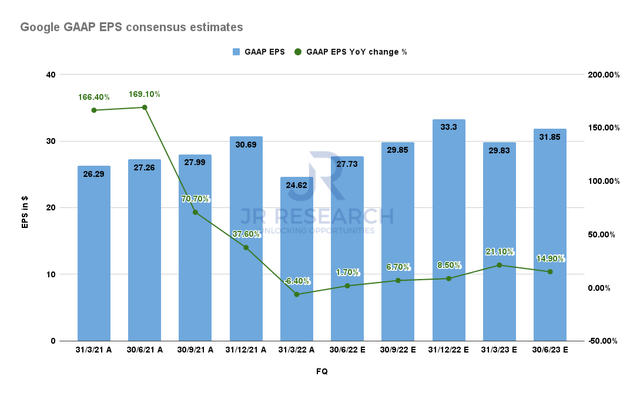

Google GAAP EPS consensus estimates (S&P Capital IQ)

Google described Q1 revenue of $68B, up 23% YoY (Vs. consensus: $67.9B, up 22.7% YoY). Nevertheless, its GAAP EPS arrived in underneath anticipations at $24.62, down 6.4% YoY (Vs. consensus: $25.64, down 2.5% YoY). Consequently, it was arguably a combined Q1 card by CEO Sundar Pichai & Crew. Yet, management was quick to spotlight the energy in Lookup, as earnings increased by 24.3%, spurred by strong advertisement paying out in retail and travel. Also, Google highlighted that overall working margins remained steady at 29.5%, as viewed higher than. Furthermore, Google has continued to commit aggressively in bodily offices, information centers, and choosing, which impacted its net profits.

But we implore traders to focus on the consistency of its functioning margins, as they shown Google’s market leadership, and nicely-diversified organization model amid the demanding ecosystem.

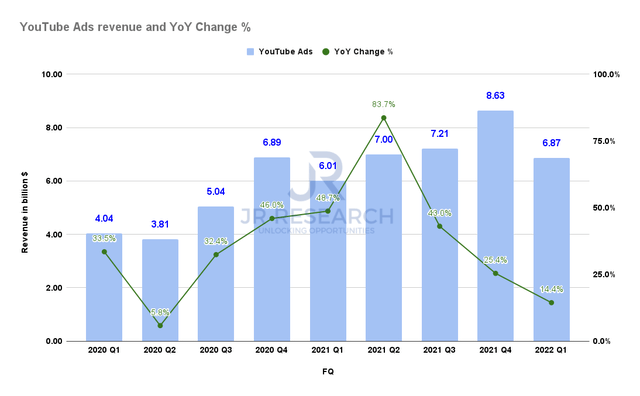

YouTube advertisements earnings (Company filings)

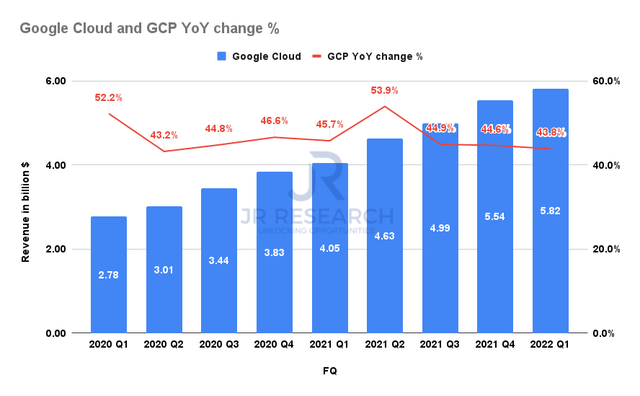

Google Cloud earnings (Firm filings)

Having said that, YouTube’s development deceleration ongoing from FQ4, as revenue improved to $6.87B, up 14.4% YoY. It was also the slowest quarter because Q2’20, as observed previously mentioned. Management was very careful not to spotlight an inherent weakness that could portend the variety of concern seen in Meta’s immediate reaction advert company.

Google emphasized that brand marketing remained sturdy whilst direct response adverts moderated. Administration stressed softer ad paying out in Europe, provided the existing crisis and weaker macros experienced afflicted YouTube’s Q1 efficiency. In addition, Google has also been testing monetization with Shorts, as it aims to up the ante in opposition to TikTok. Every day sights on Shorts amplified to 30B, quadrupling the metric over the previous yr. Nevertheless, buyers need to also anticipate some in the vicinity of-term headwinds owing to lower Shorts monetization as much more YouTube viewers shift from its extensive-kind videos.

Google Cloud carries on to impress, specified the structural shift in company IT shelling out to the hyperscalers. Its revenue enhanced to $5.82B, up 43.8% YoY. It has been instrumental in lifting Alphabet’s over-all profits, even however its operating margin remained in the crimson, at -16%. Even so, investors are encouraged to be affected person as Google Cloud scales up, as it invests far more aggressively in its multi-cloud and field verticals penetration. It also considerably improved its information cloud functionality, as it aimed to leverage the momentum collected by Snowflake (SNOW).

GOOGL Inventory Valuation Mirrored Current Headwinds

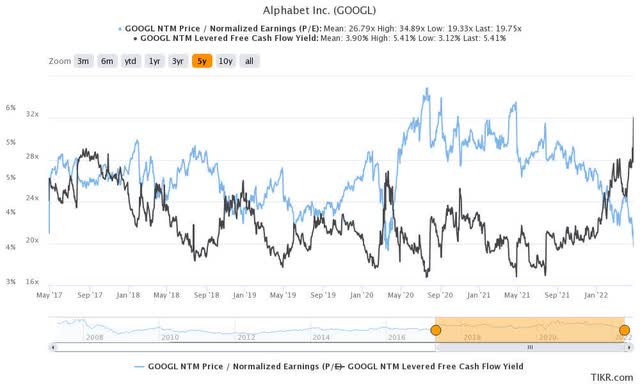

GOOGL stock NTM normalized P/E and NTM FCF produce % (TIKR)

We consider that GOOGL stock’s latest valuation has mirrored the headwinds highlighted by the enterprise in its earnings connect with. Inspite of its enormous surge in 2021, GOOGL inventory has get rid of extra than 20% of its worth from its January highs. As a outcome, the inventory past traded at an NTM normalized P/E of 19.8x (5Y mean: 26.8x). In addition, its NTM FCF yield has surged to 5.4% (5Y imply:

3.9%). For that reason, we are confident that the provide-off is overdone over the digital advertisement chief, even with its reasonable valuation and strong FCF.

Is GOOGL Stock A Purchase, Market, Or Hold?

GOOGL inventory consensus price targets Vs. inventory effectiveness (TIKR)

Notably, the inventory has ongoing to trade underneath its most conservative cost targets (PTs) for the previous six months, which is fairly astonishing. Buyers can notice that its most conservative PTs have been solid aid amounts above the previous five yrs.

Therefore, we presented a feasible clarification that the marketplace de-rated the online ad industry immediately after Meta Platforms claimed its FQ4 bombshell. Meta is scheduled to report its Q1 card on April 27. Traders have been on tenterhooks considering that Netflix (NFLX) recurring its earnings nightmare for a 2nd consecutive quarter. As a result, FB could hold GOOGL inventory back in the around time period as it rebuilds its advert tech and responds properly to TikTok’s (BDNCE) challenge. The SOTP examination on GOOGL stock also areas a significant total of emphasis on advert commit (76%). Provided Google’s market place leadership, any sector de-ranking really should impression GOOGL stock around-term valuations.

Notwithstanding, we encourage traders to increase GOOGL stock as a result of its modern weakness. But we ought to highlight that the re-score in GOOGL inventory could take a while, and for that reason, traders have to have to physical exercise persistence and prudence. Investors ought to consider a greenback-expense averaging strategy to mitigate its in the vicinity of-phrase volatility.

As such, we reiterate our Invest in rating on GOOGL inventory.

More Stories

Packing for Journey Journey

Adventure Travel to Kenya – Find out Kenya’s Most effective Kept Techniques

Experience Vacation in India